Why You Don't Stick to Your Budget

Better budgeting for intentional living

MONEYHAPPINESS

Jack Clemans

4/28/20245 min read

Budgeting Well:

Budgets are like diets. Most of us have had one, and nearly all of us have quit them.

Perhaps for this reason, budgets have been given a bad name. They are often compared to prisons, and people report feeling bullied by their budgets, especially when unexpected expenses cause them to overspend in one or several categories.

As a CFP® Professional, I know how essential budgets are to financial success, so I’ve written this article as a guide to address some of the problems with budgets and offer solutions, so more people can start budgeting and living intentionally.

“It isn't what you earn but how you spend it that fixes your class.” -Sinclaire Lewis

The Problem: “Budgeting feels like a prison, it’s too restrictive. I feel like it forces me to eat dirt, say no to hanging out with friends, and generally never leave my home except to go to work.

The Solution: You get to design your budget, so design it according to your ideal month. You should start by considering your mandatory expenses, like rent, utilities, groceries, gas, etc, and then set aside how much you would like to save, lastly, consider your voluntary spending money, and plan for all of it intentionally. We often spend more money than we mean to, so budgeting is less about restricting spending than it is about choosing to spend and therefore live intentionally.

The Problem: “I always feel SO bad when I overspend on my budget.”

The Solution: You are 100% going to overspend on your budget. Probably every month and probably in multiple categories. Life happens and it can be expensive. My recommendation would be to build intentional contingency plans; when I overspend in Category A, I will reduce my expenses in Category B, then C, D, etc. The category you cut should be your savings for that month, and if your expenses exceed your income for that month, then you know it is time to fall back on your emergency fund. However, if you find that you are consistently overspending in a given category, maybe it is time to increase your budget for that category. I include space for these contingency plans in my budgeting template.

“For where your treasure is, there your heart will be also.” - Matthew 6:21

The Problem: “I have a budget! I subscribe to one of those budgeting programs that automatically tracks my income and expenses. It is very convenient, I just haven’t logged in for a while…”

The Solution: You HAVE to be hands-on with your budget. Otherwise, the budget becomes reactive, with you looking back at how you spent over the previous month, instead of proactive with you actively taking part in how you spend throughout the month. The ideal would be to have access to your budget on your phone so you can update it whenever a purchase is made, and then review the budget periodically to ensure you’re still on track, making changes as necessary.

The Problem: “I just don’t find the information provided to be helpful.”

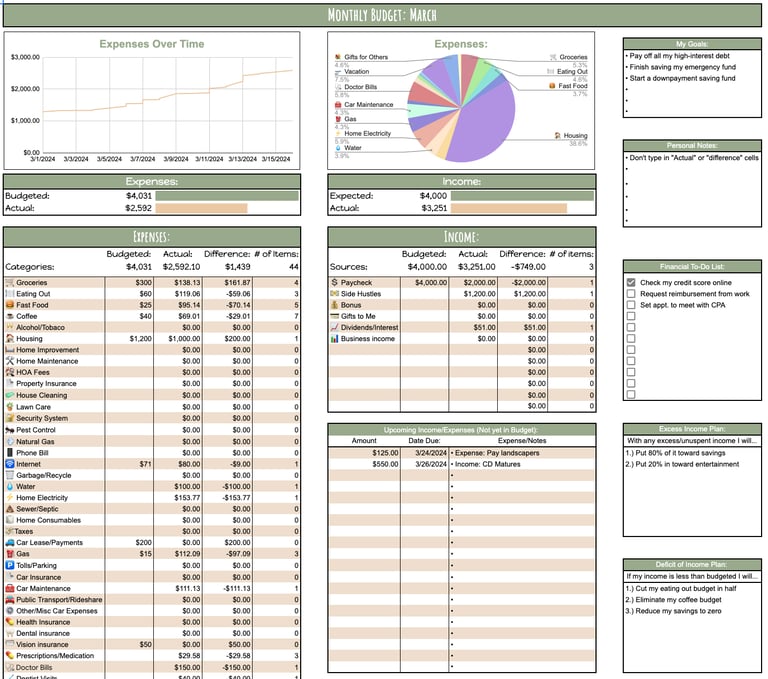

The Solution: The biggest factor for making sure your budget is able to provide useful information is your system for categorizing your income and expenses. In my experience, most folks benefit from more detailed categories. Instead of a single “food” category, I recommend breaking it up further into specific categories like groceries, eating out, fast food, coffee, alcohol, etc. This way you can more precisely pinpoint areas of high spending and make plans for adjustments if necessary. It is also good to find a method of budgeting that provides different kinds of information in different ways. In my budget, there are over 150 fully customizable categories. It also shows your total spending by category and the number of purchases made in that category, a pie chart comprised of your largest expenses, and a timeline showing your spending over time!

“If you fail to plan, you are planning to fail!” - Benjamin Franklin

The Problem: “I use a budget but I don’t seem to be making any progress financially”

The Solution: If this is the case you need to consider how you structure your income. I recommend a combination of the “Zero Base Budgeting” and the “Pay Yourself First” methods. For “Zero Base Budgeting”, you plan for every dollar of income you expect to receive that month. This includes your savings, retirement contributions, debt payoff, etc. The “Pay Yourself First” method compliments it well because it has you put money towards your financial goals as soon as you are paid. For example, if you get paid twice a month and you’ve budgeted to save $500 this month, you would immediately move $250 into savings as soon as you were paid. This way you ensure you’re benefiting from your hard work before allowing other expenses to sneak in and undermine your progress.

The Problem: “I hate spreadsheets. They are so boring.”

The Solution: While I cannot relate to this personally, because dang it, I just love spreadsheets so much, my wife tells me they are the absolute worst to even look at. Apparently, “gross” is an appropriate word for them in most cases. For that reason, I would recommend personalizing your budgeting template as much as possible. It is amazing how some colors and emojis can liven up your budgeting template and make it so much easier to keep the habit. Here is a screenshot of how I have customized my template:

The Problem: “I don’t see the point of trying to budget and cut back expenses when I can only cut back so far. Shouldn’t I instead be focusing on making more money?”

The Solution: Great question! There are two primary reasons to start with cutting expenses before you go on to try to make more money. Firstly, it is much more effective to save money than to earn more money. This is due in part because every dollar saved is $1.00, while every dollar earned is taxed, both as income and sales taxes when spent. Depending on your income level, state, and county, these taxes could take more than half of your additional income! Secondly, when you reduce your expenses, you are engaging in a process of choosing to keep in your budget that which is most meaningful to you. This not only allows you to live on less, which increases your savings and decreases what you need for retirement, but also means you are taking an active part in living intentionally which has massive psychological benefits.

If you’ve made it this far, I appreciate you reading! If you want to get started budgeting for yourself, I would recommend checking out my budgeting template. I created it with all of these problems and solutions in mind and updated it through years of use! You can find it on my website jackclemans.com. Thank you and please feel free to reach out to me on that same website if you have any questions or inquiries. Good luck and happy budgeting!

Contact Me

Jack@ClemansFinancial.com

Jack Clemans, MS, CFP®, ABFP®, CRPC®